Sugar:

Raw sugar futures have made a modest recovery over the past month. After spending much of Q2 below 12 USc/lb, prompt July futures have surged back towards 13 USc/lb. The funds have had the market under heavy pressure, building a net short position near historic levels (184,000 lots net short). Recent support from the broader commodity complex and a weakening Brazilian real have breathed life into raw sugar futures of late. Brazil continues to produce more ethanol over sugar, despite weaker WTI oil prices, with stronger demand for ethanol keeping ethanol prices buoyant. Fundamentally, the question remains if and how much sugar India will export this year. If supply from India underwhelms, it would not be unreasonable to see Brazil switch to producing more sugar. If the Indian government can solve the supply glut, then prices are expected to come under pressure again.

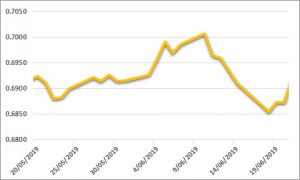

AUD:

A busy few weeks for the AUD as the Reserve Bank of Australia (RBA) cut interest rates at its latest meeting and indicated more cuts are on the way in 2019. The RBA continues to allude to weakness in the labour market and returning central inflation back to target as key drivers for cutting rates. RBA speakers in the past week have indicated a strong desire to push unemployment lower, citing that unemployment will need to fall below 4.5% before upward pressure on wages returns. This week we saw the US Federal Reserve leave rates on hold at 2.5%. A dovish tone at the Fed’s latest meeting pushed the market to price a one hundred per cent chance of a rate cut in July, with Chair Jerome Powell providing a clear easing bias and commenting that “we will act as appropriate to sustain the expansion in the economy”. The AUD continues to trade near USD 0.69. Topside resistance is expected if the market returns toward USD 0.6950.